Key Takeaways:

- Core Value: Stablecoins enable faster, borderless value transfer by combining blockchain efficiency with price stability for global payments.

- Scope of Functionality: They support settlements, treasury operations, digital commerce, and on-chain finance across both traditional and decentralized financial systems.

- Business Impact: Enterprises benefit from quicker settlement cycles, lower transaction costs, improved liquidity visibility, and always-available payment infrastructure.

- Adoption Across Sectors: Stablecoins are actively used in fintech, DeFi, Web3 platforms, and multinational businesses operating across different countries and banking systems.

- Future Trends: Stablecoins will increasingly work alongside banks and fintech platforms, supporting faster global payments without fully replacing existing systems.

Stablecoins Moving Beyond the Crypto Ecosystem

The idea of building a payments infrastructure on stablecoins is no longer limited to the cryptocurrency communities. They are beginning to play an important role in the movement of money across borders, companies and online. Look a little closer at fintech platforms today and you will see that stablecoins as payment infrastructure are already facilitating faster settlements, cheaper cross-border transfers and more efficient international transactions. These are all under the radar of most customers.Stablecoins are evolving beyond just a digital asset; they are becoming essential as financial infrastructure. Learn more about stablecoin development and how it’s transforming global payment systems.

This change is important not due to hype or conjecture. That is worthy. The flow of money is slowly becoming like the flow of data on the internet. Quick, worldwide, and always online.

What Are Stablecoins?

Stablecoins are digital currencies tied to assets like the US dollar to maintain a consistent value. Unlike volatile cryptocurrencies, they are not intended for price fluctuations or trading profits. Rather, they are to be a form of virtual currency.

Stablecoins are basically blockchain versions of traditional money. A separate elucidation of what stablecoins are and how they work explores how they maintain their peg and operate within the broader crypto economy. According to McKinsey research, public blockchain data shows total stablecoin transaction volumes reaching up to $35 trillion annually, though most of this volume reflects trading rather than true payments. This allows value to move over the internet without the delays of traditional banking.

Most stablecoins are collateralized by cash or short-term government securities. This support keeps them stable, making them useful for practical financial applications, not speculation.

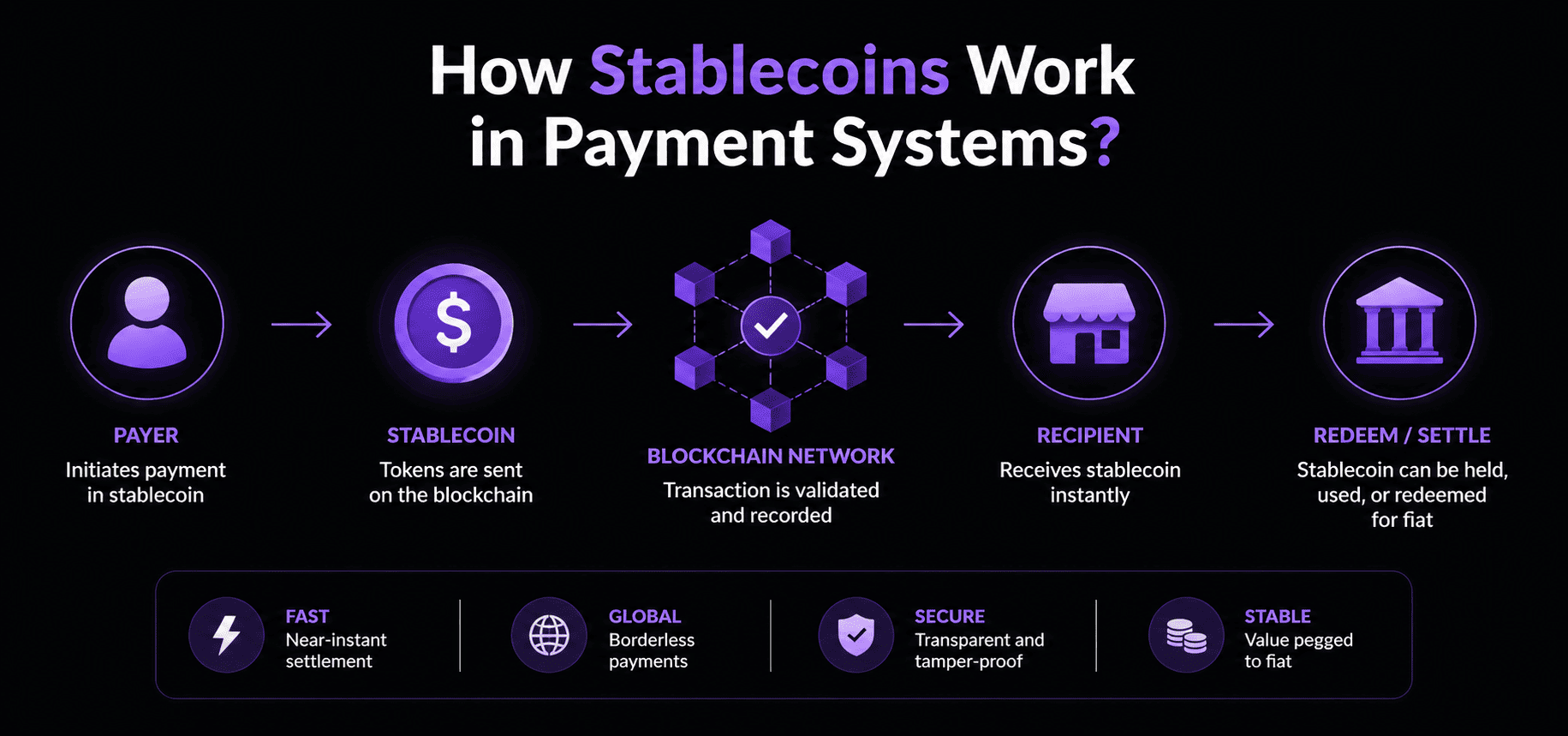

How Stablecoins Work in Payment Systems?

To understand how stablecoins enable cross border payments, is best understood by comparison with the flows of traditional banking.

International payments tend to have lots of middlemen. Each institution adds processing time, fees and compliance checks. This means that it takes days for global transfers.

Stablecoins eliminate most of this complication. The sender converts local currency to stablecoins and sends them over a blockchain network. The recipient can then instantly re-convert the stablecoins to local currency if required.

The entire process can be completed in minutes rather than days.

That is why stablecoins as global payment rails are becoming gradually relevant. They remove the need for slow financial infrastructure, allowing value to move straight between users.

Why Stablecoins Are Becoming Financial Infrastructure

The idea of using stablecoins as payment infrastructure becomes more and more popular as stablecoins solve real inefficiencies in the global financial system.

Traditional banking systems were established decades ago when most transactions were domestic and slower. Businesses operate internationally now, but the financial infrastructure has not changed at the same pace.

Stablecoins change that by adding programmable and always-available settlement layers. While stablecoins still process a small share of global daily payment volume, estimates show they support about $30 billion in transactions daily, a sign of rapid growth from almost negligible levels just a few years ago.

As such, many fintech companies are starting to look at stablecoins as financial infrastructure capable of supporting digital platforms, treasury systems and international trade, rather than as cryptocurrency assets.

Predictability is also a factor in adoption. Businesses want open, fast-settling systems. Stablecoins provide both.

Stablecoins vs Traditional Payment Systems

The difference between stablecoins and traditional banking becomes clear when you look at how money actually moves.

| Feature | Stablecoins | Traditional Banking |

| Settlement speed | Minutes or seconds | Several days |

| Availability | Always available | Limited by banking hours |

| Transaction cost | Low | High due to intermediaries |

| Transparency | Blockchain tracking | Limited visibility |

| Global access | Open internet based | Restricted banking access |

This comparison highlights why stablecoins vs traditional banking systems is becoming a key discussion in fintech. The traditional model is reliable but slow. Stablecoins are fast but still evolving in regulation and adoption. The shift from traditional payment systems to stablecoins relies heavily on blockchain interoperability. Our blockchain interoperability solutions ensure seamless transactions between different financial systems

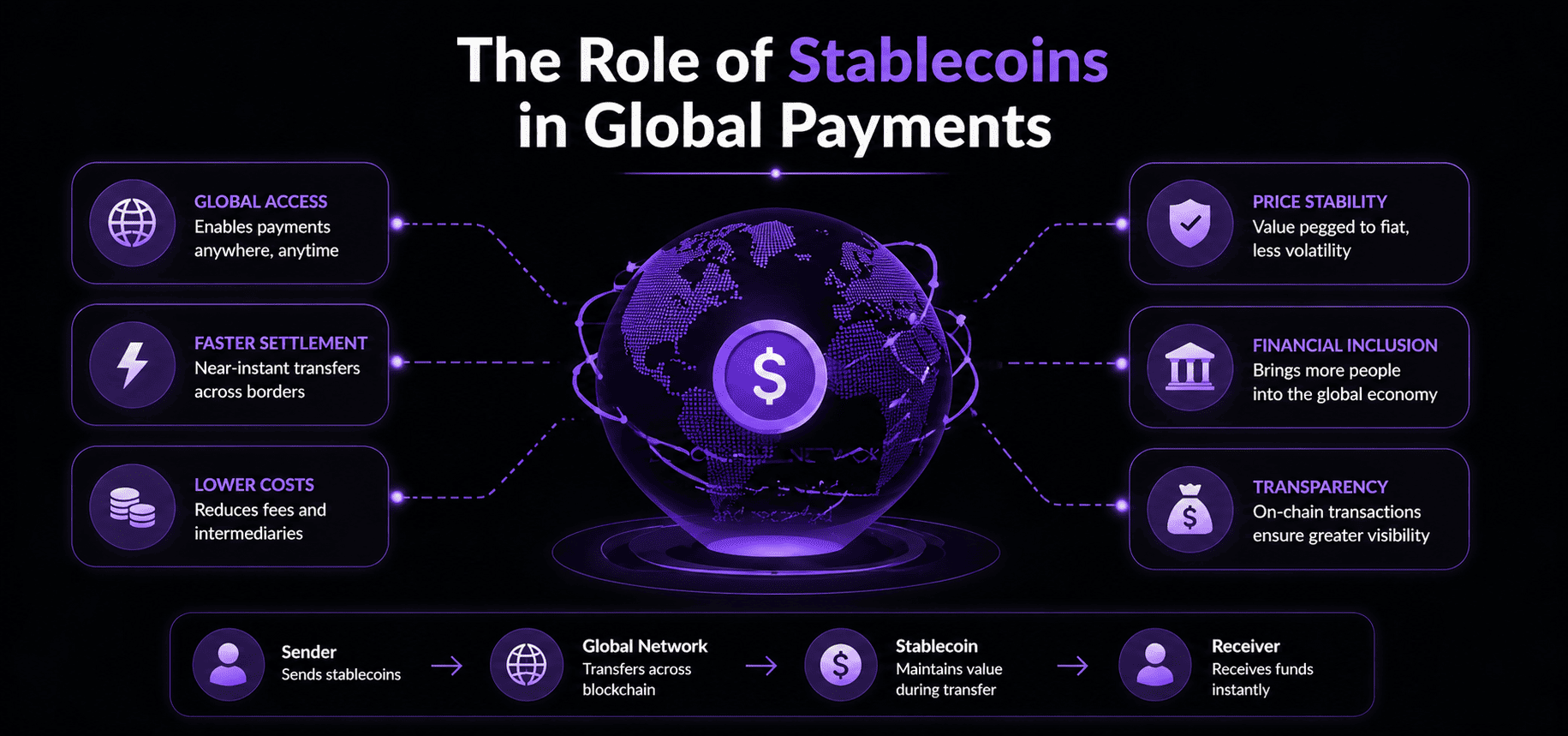

Role of Stablecoins in Global Payments

As companies seek faster and cheaper ways to move money internationally, stablecoins are becoming more important for international payments.

Businesses are using stablecoins for cross-border settlements, paying suppliers and running international payroll. Remote workers and freelancers are also winners, getting paid almost instantly, with no costly transfer fees. Cross-chain interoperability plays a crucial role in facilitating stablecoin transactions across borders. To understand how smart contracts power this, check out our Cross-Chain Smart Contract services.

Cost-effectiveness is one of the biggest advantages. Forbes reports that stablecoins can reduce remittance fees from about 6.49% to under 1% in certain corridors, which could save tens of billions of dollars annually if widely adopted. Traditional overseas payments involve multiple banking fees and layers of currency conversion. Stablecoins remove intermediaries and significantly lower these costs.

That’s why stablecoin adoption in global markets is flourishing constantly, particularly in countries where the banking system is expensive or slow.

Stablecoins in DeFi and Web3 Ecosystems

Decentralized finance is powered by stablecoins. Most lending, borrowing and trading activities are done in stablecoins which are stable in an otherwise unstable environment.

DeFi systems use stablecoins as:

- The chief medium of exchange.

- Collateral for lending procedure.

- Liquidity on decentralized exchanges.

Stablecoins are the default digital currency in the Web3 ecosystem. Stablecoins provide pricing stability and transactional consistency for decentralized apps, blockchain games, and NFT marketplaces.

Most of the Web3 financial systems simply cannot function at scale without stablecoins. Stablecoins are pivotal in decentralized finance (DeFi) platforms. Learn how our Web3 development services help integrate stablecoins into your decentralized applications

Stablecoins for Enterprise Payment Solutions

International financial transactions are made easier by the use of stablecoins, which is why companies are increasingly exploring custom stablecoin development as a foundation for enterprise payment solutions. Businesses are no longer just using off-the-shelf digital assets but are building tailored stablecoin systems designed for their treasury, payroll, and cross-border settlement needs, often leveraging blockchain development expertise.

Companies that operate internationally often face long settlement cycles, complicated treasury management systems and foreign exchange fees. All of this can be facilitated by stablecoins.

For instance, real world enterprise use cases include global payroll distribution, payments to suppliers, internal fund transfers, and cross-border invoicing.

Finance teams are focused on operational efficiency. It accelerates settlement, so you’re not relying on slow financial systems and can better manage liquidity.

Stablecoins vs CBDCs: Key Differences

Stablecoins and central bank digital currencies are often discussed together because they both are the next evolution of digital money. They do, however, rest on quite different principles. The private sector created stablecoins to help make online shopping, blockchain apps and international digital payments easier. Their growth has been driven largely by real-world demand for faster, more flexible ways to pay.

CBDCs, on the other hand, are issued and controlled by central banks with a focus on monetary policy and domestic financial stability. They are designed to upgrade national payment systems, not to open global currencies. Both models may co-exist in the future but stablecoins are seeing wider use in the real world for cross-border digital payments. The main differences between CBDCs and stablecoins are shown in the table below.

| Aspect | Stablecoins | CBDCs |

| Issuing authority | Issued by private companies or decentralized systems | Issued and controlled by central banks |

| Primary purpose | Designed for global payments and digital commerce | Focused on domestic payments and monetary policy |

| Geographic scope | Global and borderless by design | Mainly limited to national or regional use |

| Speed of innovation | Evolve quickly based on market demand and technology | Move slowly due to regulatory and policy processes |

| Integration | Easily integrate with fintech, DeFi, and Web3 platforms | Integrated mainly within government and banking systems |

| Current adoption | Widely used in global digital payments and crypto markets | Still in pilot or early rollout stages in most countries |

Risks and Challenges of Stablecoins

Stablecoins are expanding fast but are also very risky and should not be overlooked.

Transparency of reserves is one of the main problems. Customers want to know that all stablecoins are backed by real assets. Without proper audits, trust might be compromised.

Another problem is the uncertainty of the rules. Different countries are working on different frameworks, making global adoption tricky.

There are also technical problems, such as liquidity stress during market volatility and weaknesses in smart contracts.

Consequently, stablecoin regulation and compliance trends have emerged as a major topic of global concern. Regulators are trying to maintain stability, security and transparency without stifling innovation. With the growing adoption of stablecoins, ensuring security is crucial. Learn how our blockchain security solutions can help safeguard your stablecoin infrastructure.

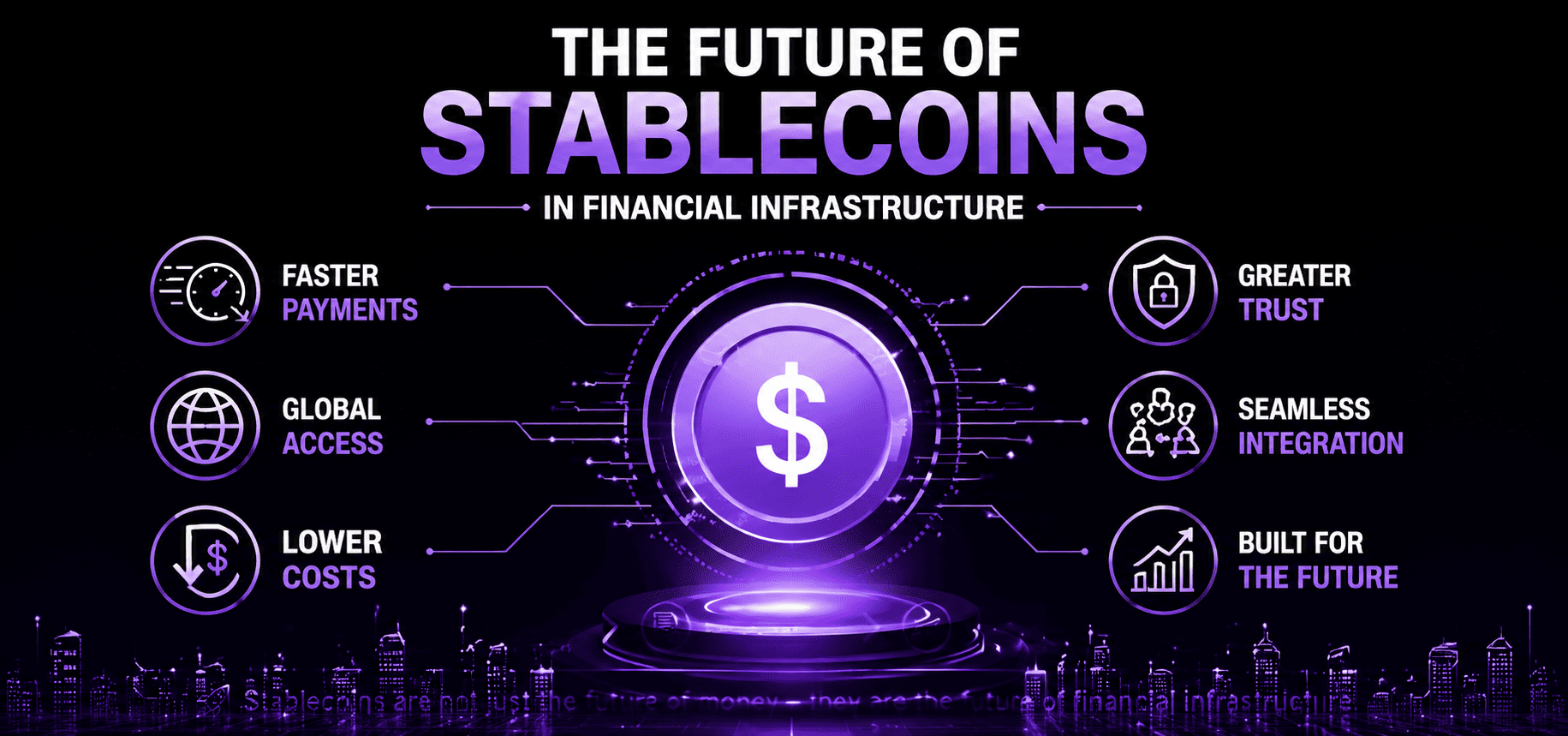

Future of Stablecoins in Financial Infrastructure

The future of stablecoins in fintech is more about integration than disruption.

Stablecoins are more likely to coexist as a settlement layer for international transactions, rather than replacing existing mechanisms.

We are already witnessing the first signs of this shift. Payment companies are building stablecoin rails. Fintech apps are offering instant foreign transactions. Banks are experimenting with tokenized deposits and settlement systems on blockchains. As stablecoin infrastructure moves from experimentation to production, organizations often rely on technology firms like Techfyte to support the engineering and deployment of blockchain-based payment systems.

Stablecoins as payment infrastructure can become as common as wire transfer or card networks, but faster and better.

The actual modification is greater than tech. It is behaviour. Businesses and people are beginning to expect money to move at the speed of information. Businesses evaluating modern payment infrastructure should assess whether stablecoins fit their regulatory, operational, and cross-border payment needs.

Final Thoughts

Stablecoins are more than just a crypto innovation. They are becoming an important part of the financial infrastructure of today.

With the world’s trade becoming more digital, the need for quicker and more efficient payment solutions is increasing. Stablecoins fill that gap by allowing quick, inexpensive and international transactions.

The change has already begun. Also, with increased use, stablecoins as payment infrastructure will probably be one of the most essential segments of the future financial system.

As stablecoins evolve into mainstream financial infrastructure, blockchain-based payment systems are playing a key role. Learn more about how our blockchain payment systems are shaping the future of payments.

Frequently Asked Questions

1. What are stablecoins in the payment infrastructure?

Stablecoins are digital currencies which are pegged to a stable value, but can still be transferred quickly and cheaply over blockchain networks. They act as a trusted settlement layer in payment infrastructure, facilitating cross-border money transfers without the pain and delay of traditional banking infrastructure.

2. How do stablecoins improve global payments?

Stablecoins can settle transactions in minutes rather than days, dramatically accelerating the movement of money across borders. They also cut down on transaction costs and increase transparency for international payments by eliminating several middlemen.

3. Are stablecoins replacing traditional payment systems?

Stablecoins are gradually being integrated into traditional payment rails rather than replacing them. Stablecoins are used by banks, fintech companies and payment providers to improve payment efficiency, liquidity management and cross-border settlement.

4. What industries use stablecoins?

Stablecoins are employed in fintech, e-commerce, gambling and digital platforms for quicker and more efficient payments. Multinational corporations use stablecoins for their treasury work, paying suppliers, payroll etc across the globe.

5. What is the difference between stablecoins and CBDCs?

Stablecoins are supposed to be used for digital transactions across borders and are issued by private companies or decentralized systems. Central banks issue CBDC, mainly used for monetary policy objectives and domestic payment infrastructure.

6. Are stablecoins safe for enterprise use?

When used within regulatory frameworks and backed by transparent reserves, stablecoins can be safe for business use. Businesses still require risk controls, issuer due diligence and proper compliance procedures.