Key Takeaways

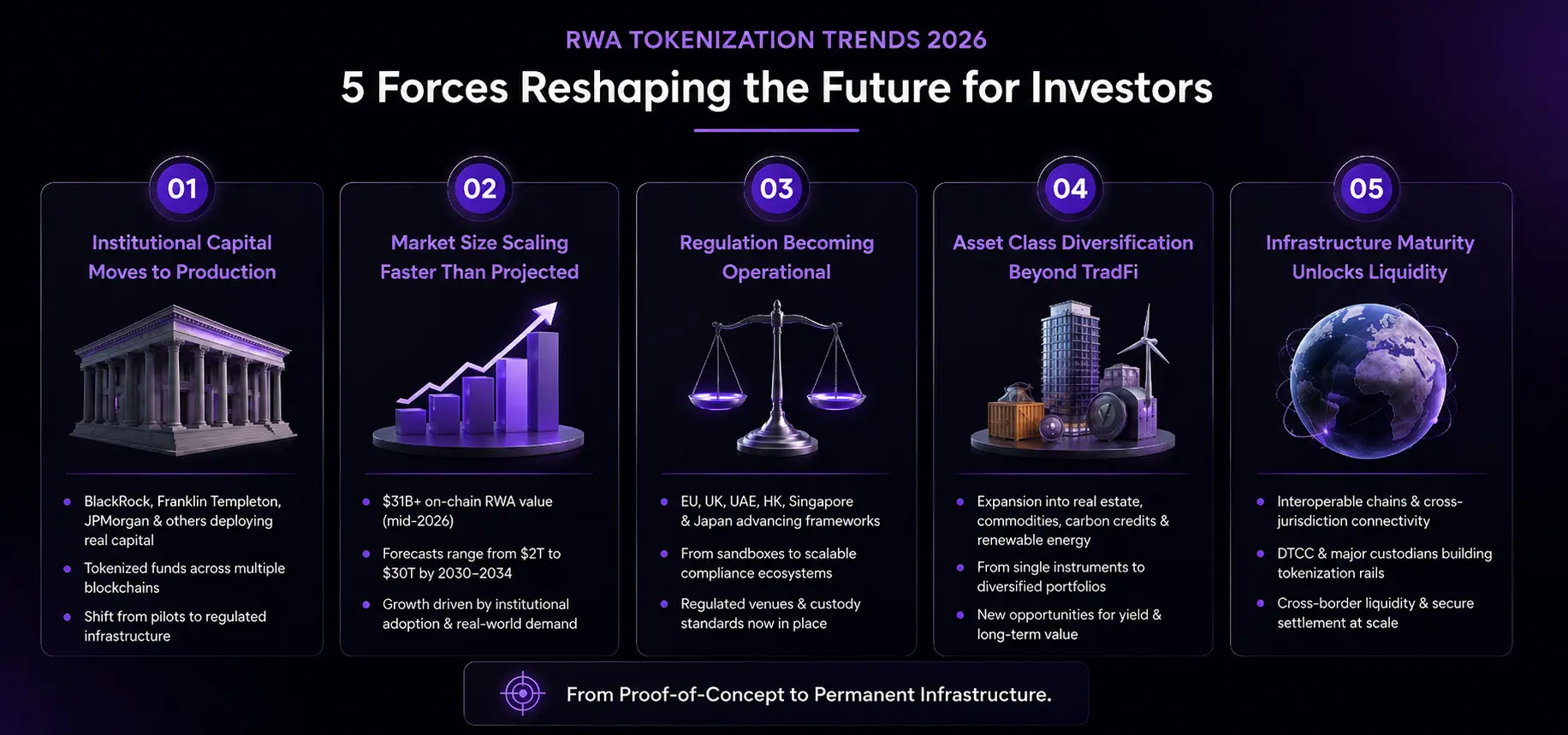

- Institutional Shift: RWA tokenization has entered the institutional era, with on-chain asset value growing from approximately $5 billion in early 2024 to over $31 billion by mid-2026.

- Major Players: BlackRock, Franklin Templeton, JPMorgan, Fidelity, and Apollo are moving from pilot projects to large-scale production deployments.

- Market Growth: Market forecasts for tokenized assets continue to rise, with estimates ranging from $2 trillion to $30 trillion over the next decade as adoption accelerates.

- Regulatory Maturity: Regulatory frameworks across the EU, UK, UAE, Singapore, Hong Kong, and Japan are evolving from experimental sandboxes to operational compliance ecosystems.

- Asset Expansion: Asset tokenization is expanding beyond private credit and treasuries into real estate, commodities, carbon credits, and renewable energy assets, supported by maturing cross-border infrastructure.

RWA Tokenization Trends 2026: What’s Changing and Why It Matters for Investors

Finally, real-world asset tokenization has reached a milestone that pilots never could: production scale at a large institutional level. The on-chain value of RWAs, excluding stablecoins, surged from roughly $5 billion in early 2024 to more than $31 billion as of mid-2026, with tokenized U.S. Treasury securities comprising almost $13 billion.

The acceleration is notable because 2026 is the year that regulatory sandboxes began to create real rulebooks, institutional money managers stopped testing and began to deploy real capital, and infrastructure providers began to harden the settlement rails on which those flows depend.

These RWA tokenization trends 2026 indicate an industry moving from proof-of-concept to permanent infrastructure that asset managers can actually insure.

Investors comparing the broader market can also review real-world asset tokenization use cases to understand where adoption is moving beyond financial instruments.

In this post, we look at five forces reshaping the landscape for institutional investors: capital deployment, market size forecasts, operational regulation, asset-class diversification, and cross-border liquidity infrastructure.

Trend 1: Institutional Capital Moves from Pilots to Production

BlackRock’s BUIDL fund launched in March 2024 and now has $2.5 billion-plus in assets under management across eight or more blockchain networks. It was accepted as off-exchange collateral on a major derivatives venue in late 2025.

Franklin Templeton has added eight chains to its BENJI fund, and JPMorgan is set to introduce its own tokenized money market fund, MONY, in December 2025 with an initial $100 million for qualified investors. Similarly, Fidelity and Apollo have created similar products, which are among the most obvious RWA tokenization developments to come, given that they use regulated balance-sheet capital instead of speculative flows.

It is not appetite that has changed; it is infrastructure preparedness. Custody arrangements and institutional custody solutions have evolved to the point that large banks feel comfortable deploying balance-sheet items on public chains instead of private test environments.

This shift puts tokenized bonds and equities into the institutional arsenal, with the liquidity and regulatory credibility that pilot programs could never have. BlackRock CEO Larry Fink has reiterated his conviction that most financial assets will eventually be tokenized and has put his firm’s capital behind that view.

Trend 2: The Market Size Is Scaling Faster Than Projected

Forecasts for RWA tokenization market size 2026 and beyond vary depending on what analysts count, but the direction is unmistakable. Earlier 2023-era estimates clustered near single-digit trillions; the 2025–2026 revisions moved meaningfully higher as adoption data backed up the theory.

Here is how the major projections stack up:

- McKinsey: $2 trillion in tokenized financial assets by 2030, representing the most conservative baseline among major consultancies.

- Boston Consulting Group and ADDX: $16 trillion by 2030, reflecting a faster adoption curve driven by institutional entry and regulatory clarity.

- Standard Chartered: $30 trillion by 2034, the most aggressive forecast, predicated on tokenization becoming the default settlement layer for cross-border capital flows.

- Ripple and BCG: $18.9 trillion by 2033, sitting between the mid-range and high-end estimates, with particular emphasis on Asia-Pacific growth.

Where Current Volume Is Concentrated

Private credit remains the largest single segment of current tokenized value, but treasuries, corporate bonds, and institutional alternative funds have all exceeded the $1 billion on-chain threshold.

These RWA tokenization market size projections for 2026–2030 reflect broader RWA market trends, such as capital concentrating first in liquid, yield-bearing instruments before spreading into less liquid asset classes.

Why the Numbers Keep Being Revised Upward

Institutional involvement altered the modeling. When BlackRock, Franklin Templeton, and JPMorgan put balance-sheet products on-chain rather than conducting sandbox experiments, forecasters revised their assumptions about adoption velocity.

The revised projections now assume tokenization will become infrastructure rather than a niche product category, and data from mid-2026 supports this assumption.

Trend 3: Regulatory Frameworks Are Becoming Operational, Not Just Announced

The EU’s DLT Pilot Regime struggled for adoption during its first two years, with only a few authorized infrastructures and volume caps that were too low to justify investment. That changed through 2025, as the European Commission moved to extend the regime and ESMA’s formal review demanded clarity on its long-term viability.

The UK moved faster: the FCA and Bank of England’s sandbox now has 16 firms working toward live issuance, and in May 2026, the regulators issued a joint Call for Input on tokenized securities and settlement.

Hong Kong, Singapore, and the UAE have all developed licensing pathways for tokenized securities issuance, while Japan plans to reclassify crypto-assets as financial products in 2026, aligning capital gains treatment with traditional securities.

Operational regulation allows licensed venues, enforceable custody rules, and compliance reporting teams to actually underwrite, which distinguishes this cycle from previous pilot-heavy years.

Regulatory-compliant token design has shifted from advantage to table stakes for institutional-grade platforms.

For UAE-focused projects, investors can also compare real estate tokenization in the UAE to understand how regional regulation is shaping tokenized property launches.

Trend 4: Asset Class Diversification Beyond the Usual Suspects

Private credit and U.S. Treasuries were the dominant instruments in the early RWA market due to the ease of standardization and pricing. Diversification is visible in 2026: real estate tokenization has moved from isolated experiments to live secondary marketplaces, with frameworks supported by Dubai’s regulator and many EU states issuing fractional property tokens at scale.

Issuers are also favoring commodity tokenization, carbon credit tokenization, and renewable energy certificates for sustainable assets.

Businesses planning a property-focused platform can also review real estate tokenization platform development to understand the business model, features, cost, and technical stack behind these products.

This diversification matters for portfolio construction, not just headline growth. Instead of a single yield-bearing instrument packaged together, asset managers looking for on-chain diversification need correlated and uncorrelated asset classes that can be combined the same way traditional portfolios are constructed.

RWA tokenization is moving from being a niche treasury instrument to an investable asset class beyond treasuries and private credit.

Trend 5: Infrastructure Maturity Unlocks Cross-Border Liquidity

Interoperability between chains and across jurisdictions is increasingly becoming practical, rather than theoretical. The Depository Trust & Clearing Corporation, which manages assets exceeding $114 trillion, is preparing to launch a tokenization service for real-world assets following a handful of production trades.

Major custodians are building bridges so tokenized assets can move across networks without fragmenting liquidity, and secondary market liquidity is coalescing around regulated venues, precisely what institutional allocators require before deploying larger ticket sizes.

None of this works without trust in the underlying code: standardized token frameworks and independent security evaluations of smart contracts are now required to participate, not optional.

All new platforms now have cross-border distribution as a design requirement from day one. Industry trackers like the State of RWA Tokenization 2026 report study show this infrastructure is growing fast.

High-volume platforms can also explore Layer 2 blockchain development when lower-cost settlement and faster transaction processing are required for institutional-scale tokenized assets.

What This Means for Investors and Asset Managers

2026 is the year that investors looking at exposure move from asking “does tokenization work?” to “which provider does it credibly?”

Before beginning to analyze yield or fees, ask any prospective RWA tokenization development company about its audit history, how it is licensed by regulators, and what chains and custodians it is currently integrated with.

The cost of waiting is real, as liquidity is concentrated on early-mover platforms; but the cost of moving early with an unaudited or unregulated supplier is even more expensive.

The RWA tokenization crypto 2026 trends are moving toward compliance-first infrastructure and away from speculative experimentation. That means the providers worth underwriting are those that can already show live regulatory licenses, not roadmaps that promise them.

For companies comparing build paths, how to tokenize real estate on blockchain is also useful for understanding the practical steps behind ownership structuring, smart contracts, and investor onboarding.

Concluding Note

The common thread in all of the above RWA Tokenization Trends 2026 is that tokenization has moved from concept to infrastructure.

It is unusual in financial technology cycles to have institutional capital, regulatory clarity, and cross-chain plumbing all align. By the end of 2026, the market’s center of gravity is expected to tilt even further toward operational deployment, with regulatory-compliant platforms and diverse asset coverage setting long-term companies apart from the competition.

For enterprises and asset managers ready to move from strategy to execution, Techfyte’s asset tokenization services provide the technical foundation to build compliant, scalable, and investor-ready tokenization platforms.

Frequently Asked Questions

1. What are the most important RWA tokenization trends 2026 investors should watch?

The defining RWA tokenization trends for 2026 are institutional capital transitioning from pilots to production, market size predictions being dramatically revised upward, and regulatory frameworks becoming operational.

BlackRock’s BUIDL fund has hit $2.5 billion, many jurisdictions now have legal paths to tokenization, and custody and secondary market infrastructure has matured enough to allow balance-sheet capital to flow on-chain at scale.

2. What is the RWA tokenization market size 2026, and how fast is it growing?

The on-chain RWA value had grown to more than $31 billion by mid-2026, up from around $5 billion in early 2024.

The RWA tokenization market size forecast for 2026–2030 varies widely. McKinsey sees $2 trillion by 2030, BCG and ADDX project $16 trillion, and Standard Chartered estimates $30 trillion by 2034, with current flows powered by private credit and tokenized U.S. Treasuries.

3. How are RWA market trends shifting beyond private credit and treasuries?

RWA market trends point to diversification, with real estate tokenization, commodities tokenization, carbon credits, and renewable energy certificates gaining momentum in 2026.

This growth takes tokenization from a specialist treasury tool to an investable asset class that allows for diverse portfolio construction, rather than a single yield-bearing instrument.

4. What should investors ask an RWA tokenization development company before committing capital?

Require independent audits of their smart contracts, proof of licensing by regulators in at least one major jurisdiction, and a transparent list of the blockchains and custodians they connect with.

An RWA tokenization development business without operational approvals or audited infrastructure is not ready for institutional funding.

5. How are RWA tokenization crypto 2026 trends different from earlier market cycles?

Previous cycles were based on pilots and guesswork. Trends for RWA tokenization crypto 2026 include compliance-first infrastructure, such as operational regulations in the EU, UK, UAE, and Asia, institutional solutions from BlackRock, Franklin Templeton, and JPMorgan, and cross-chain interoperability built into platforms from the start.

The market has moved past proof-of-concept into permanent, underwritable infrastructure.